TL;DR — The halal way to transact a UAE VIP number

- A UAE mobile number transaction is structurally halal when there is no riba (interest), no gharar (uncertainty), no maysir (gambling) — and the asset is transferred tangibly through the carrier.

- The buy flow is five steps: browse → contact → agree on a spot price → visit the carrier store together → complete TDRA ownership transfer.

- The sell flow mirrors it: list honestly → reply with full disclosure → negotiate one fair price → meet at the carrier store → hand over ownership for cash settlement.

- Premium 786 numbers in 2026 trade between AED 10,000 (entry) and AED 500,000+ (collector tier). Pricing must be transparent and spot-settled — no installments with interest.

- The transaction is finalised when the SIM is issued in the buyer's name at the carrier, witnessed by the operator. Allahu A'lam — consult a qualified scholar for your personal ruling.

1. What "halal-compatible" means for a UAE mobile number

Note on terminology: Throughout this guide, "mobile number" and "cell phone number" refer to the same thing — a TDRA-registered UAE SIM with a unique 10-digit identifier (050, 052, 054, 055, 056, 057, 058 prefixes). International buyers more often search using "cell phone number"; the halal framework applies identically to both terms.

Is Buying a Phone Number Halal?

Riba · Gharar · 786 — 30-second answer

Already know it's halal? Watch the 30-second proof.

Quick recap of the halal framework before you dive into the buy/sell/list steps. Hit play, then continue scrolling.

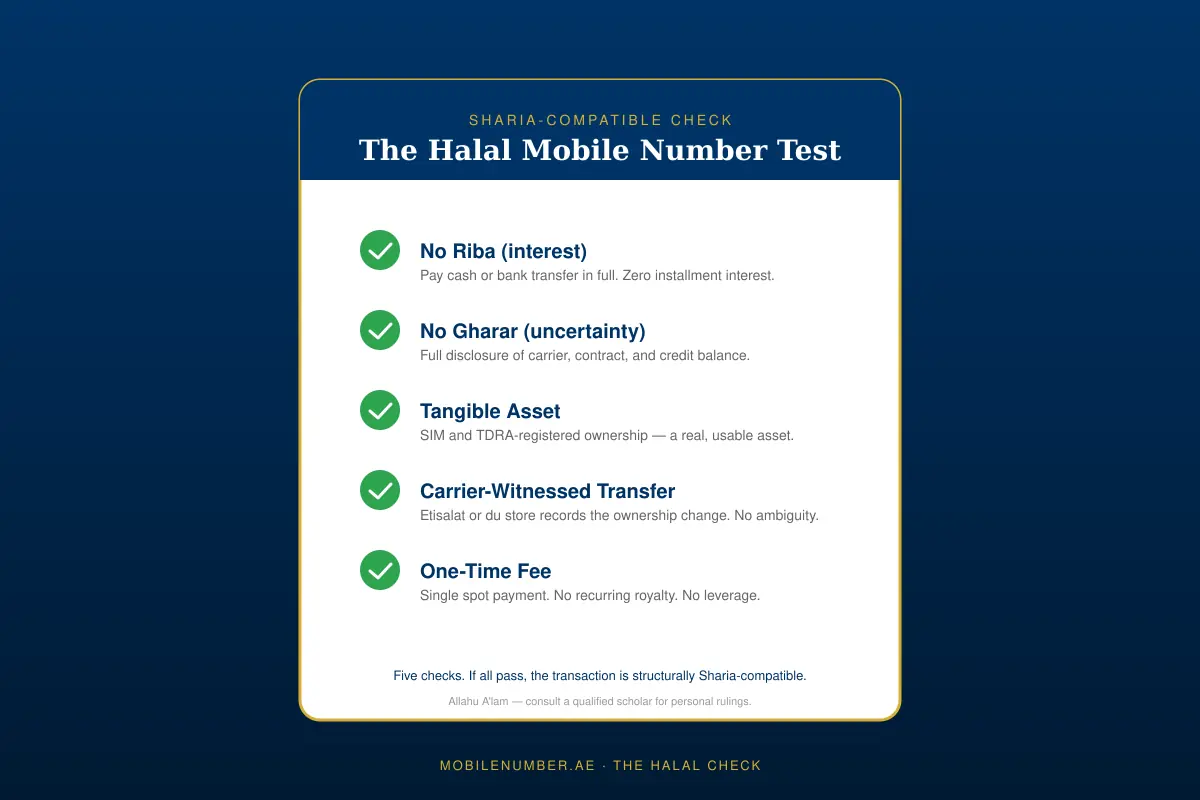

A halal-compatible UAE mobile number transaction is a buy or sell that satisfies four classical Islamic finance principles applied to a tangible asset: no riba (no interest charges or interest-bearing installments), no gharar (no significant uncertainty about the asset, the price, or the timing), no maysir (no gambling-style pricing or speculative wagering), and qabd — actual possession and constructive delivery of the asset through the legitimate ownership channel, which in the UAE means the Telecommunications and Digital Government Regulatory Authority (TDRA) ownership transfer recorded at an Etisalat or du carrier store.

The mobile number itself is treated as a usufruct attached to a SIM — a real, registered asset that the holder uses, controls, and can transfer. That is the same structural logic Sharia scholars apply to leasehold contracts, domain names, and other intangible-but-controlled assets. For the foundational reasoning, see the companion piece Halal Investment in the UAE: Why VIP Mobile Numbers Are a Sharia-Friendly Asset — this article is the procedural follow-up.

A halal transaction is finalised when the SIM is in the buyer's name — not when WhatsApp says "deal".

The four-test framework

- Tangible: Does the buyer take real possession via TDRA registration? Yes — the SIM is reissued in their name on the spot.

- Transparent: Is the price agreed, fixed, and disclosed before the meeting? Yes — one price, paid once.

- Witnessed: Does a neutral third party (the carrier operator) record the transfer? Yes — that is the carrier store's role.

- Interest-free: Is payment made in spot cash or a single bank transfer? Yes — no monthly carry, no compounding fees.

If all four checks pass, the structure is sound. Whether a specific personal situation is permissible — for example, the source of the funds, prior agreements, or intent — remains a matter for a qualified scholar to advise on.

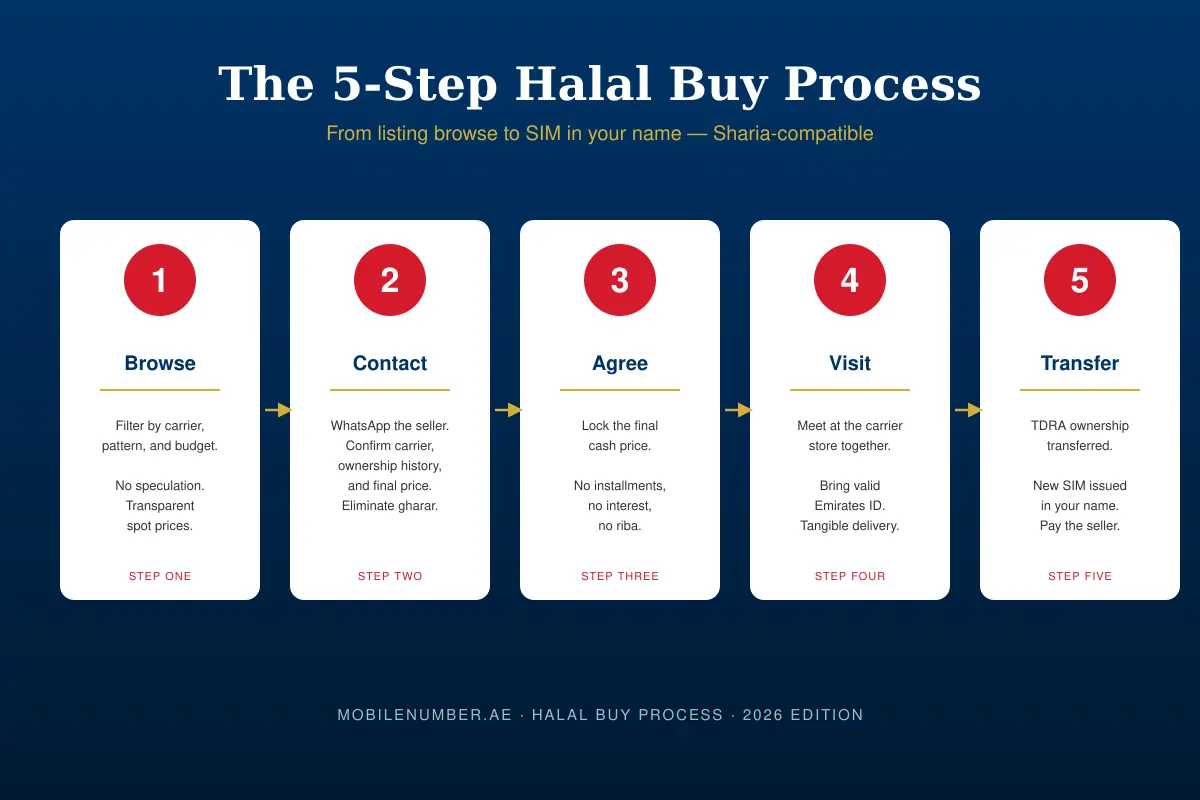

2. Buy process at a glance — the 5 mandatory steps

The halal buy process is a five-step procedure designed to satisfy Islamic finance principles at every checkpoint. Each step has a specific halal compatibility rule attached. Skip a step or fudge the order and the transaction loses its structural soundness.

- Browse halal-compatible listings filtered by carrier, prefix pattern, and budget.

- Contact the seller through the marketplace (WhatsApp or in-platform messaging) and ask the disclosure questions.

- Agree on a single, transparent, cash-settled price — no installments, no escrow with interest.

- Visit the original carrier store with both Emirates IDs and the agreed payment ready.

- Transfer ownership via TDRA-recognised process — new SIM is issued to the buyer; payment is released to the seller.

Read each step below for the exact halal checkpoint. If anything is off, pause and reassess before committing.

3. Step 1: Browse halal-compatible listings

Browsing is the discovery step where the buyer filters available numbers without any binding commitment. The halal rule here is simple: no speculation, no fishing for irrational pricing. Open the marketplace, set your filters, and look at real listings with disclosed sellers.

What to filter on

- Carrier: Etisalat (050, 054, 056) or du (052, 055, 058). The carrier determines the store you'll visit.

- Pattern: repeating digits (XX-XXX-XX), sequential runs (12345), the 786 prefix, or symmetrical mirrors. Pattern drives price.

- Budget: set a hard maximum before you start. Halal pricing avoids emotional escalation.

- Prefix age: older prefixes (050, 052) tend to command a premium because they predate the carrier expansions.

For pattern intuition and current market rates, the companion article UAE Mobile Number Market Prices 2026 — What Buyers Pay & Sellers Earn walks through real transaction bands. Treat that data as a sanity check, not a target.

The halal checkpoint at Step 1

While browsing you are not yet in a contract. There is no riba, no gharar, no obligation. The check is about intent: are you researching with a legitimate use case (personal, business, family), or are you trying to corner a pattern for speculative resale? Sharia scholars are comfortable with reasonable resale intent if the asset is real and the price is fair. They are uncomfortable with manipulative cornering of the market.

"Browsing is not a contract. Save listings, compare, and walk away if the patterns feel forced. The market will still be there tomorrow."

4. Step 2: Contact the seller via WhatsApp

Contacting the seller is the disclosure step. The halal rule here is to eliminate gharar — the buyer must understand exactly what they are about to acquire before any money changes hands. WhatsApp is the dominant UAE channel for this, both because of carrier-store practicality and because it produces a written record.

The four mandatory disclosure questions

- Which carrier is the number on, and has it ever been ported? The buyer needs to visit the correct carrier store. A previously ported number can complicate transfer.

- Is the line on a postpaid contract, a prepaid SIM, or in a corporate package? Each has a different transfer path. Corporate releases need extra paperwork.

- Is there an outstanding credit balance or unpaid bill? Any open balance must be settled before transfer. The seller normally clears this; the buyer must verify in writing.

- When was the SIM last used, and is the original holder available to visit the store? Inactive SIMs can be reclaimed by the carrier. The original holder's physical presence is required at transfer.

If the seller answers all four clearly and consistently, gharar is eliminated. If answers are evasive, fragmented, or change between messages, that is a halal red flag — pause the transaction.

Verification tip

Ask the seller to send a screenshot of their carrier app showing the number and their name partially masked. This is a normal pre-transaction check and a reasonable seller will provide it. For deeper scam protection, see How to Buy and Sell VIP Mobile Numbers Safely in the UAE.

5. Step 3: Agree on a final, transparent price

Price agreement is the most halal-sensitive step. The rule: one price, paid once, in full, in cash or by single bank transfer. No interest-bearing installments, no escrow that charges a percentage, no leveraged payment plans.

What is halal in price negotiation

- A single back-and-forth conversation where buyer and seller reach a fair number.

- A discount in exchange for spot-cash settlement (this is permissible — it is not interest).

- A holding deposit (down payment) of a defined amount, with the balance paid at the carrier store on the same day.

- A neutral escrow service that charges a flat fee for holding funds — the fee is a service charge, not interest.

What crosses into haram territory

- Splitting the price into monthly installments where the total is higher than the spot price — that is structurally riba.

- Tying the final price to a future event ("I'll pay you more if the number appreciates") — that is gharar and maysir combined.

- Using an escrow service that holds the funds in an interest-bearing account and pays interest to either party.

- Speculative bidding wars where the price is being driven by emotion rather than the asset's market value — scholars caution against participating in maysir-style auctions.

If the seller asks for "monthly installments with a little extra", politely decline. That little extra is riba.

Halal negotiation script

A clean halal negotiation reads like this: "My maximum is AED X. I can pay it in full by bank transfer at the carrier store today or tomorrow. If we agree, I will not negotiate further. Please confirm yes or no." One offer, one price, one settlement date. Clean.

6. Step 4: Visit the carrier store together

The carrier store visit is where the abstract contract becomes a tangible asset transfer. The halal rule: qabd — actual possession is taken by the buyer, witnessed by a third party (the carrier), with both parties physically present holding valid Emirates IDs.

What to bring

- The buyer's original Emirates ID (must be valid, not expired).

- The seller's original Emirates ID (the name registered to the SIM).

- The agreed payment, either in cash within the carrier store's transaction limit, or via instant bank transfer that can be confirmed on the spot.

- The SIM card or the eSIM details, depending on the line type.

- Any UAE residence or family book documentation the carrier may request for high-value premium numbers.

Which store to visit

Always visit a main Etisalat (e&) or du business centre — not a small kiosk. Main branches have the authority to process ownership transfers on the spot. Kiosks may only sell SIMs and recharge cards. For a deep walkthrough of the transfer paperwork itself, see How to Transfer Mobile Number Ownership in UAE — Complete 2026 Process Guide.

The halal moment

The moment the carrier operator scans both Emirates IDs, prints the ownership transfer form, has both parties sign, and prints a new SIM in the buyer's name — that is qabd. That is the halal-finalising act. Pay the seller right after, not before. The written record (the transfer receipt) is the proof the asset has changed hands.

"Money before SIM is gharar. SIM before money is generosity. Both at the carrier store at the same time is halal."

7. Step 5: Complete TDRA ownership transfer

The TDRA ownership transfer is the regulatory layer that records the change. Inside the carrier store, the operator submits the transfer to the carrier's TDRA-linked system. Once accepted, the number is permanently registered to the buyer's Emirates ID number.

What you receive

- A new SIM (physical or eSIM QR) provisioned to the buyer's name.

- A printed transfer receipt with the carrier's reference number, both parties' Emirates ID numbers (last digits), and the operator's signature.

- An SMS to the new owner's secondary contact confirming the transfer.

- Access to the carrier app (e& My e&, du Smarthub) where the number now appears under the buyer's account.

What the seller receives

- Confirmation that the line is no longer in their name — they are released from any future billing or liability.

- The agreed payment, settled in full on the spot.

- A receipt copy for their records (recommended to keep for at least 12 months).

The regulatory framework for this is governed by the Telecommunications and Digital Government Regulatory Authority. Their published consumer rights cover the legitimacy of ownership transfers between consenting parties with valid Emirates IDs.

8. Sell process — the seller-side flow

The sell process is the mirror of the buy process, with seller-specific halal responsibilities at each step. Selling a UAE mobile number is halal when the seller represents the asset honestly, agrees on one fair price, and delivers tangible ownership at the carrier store.

- List the number on a reputable marketplace with an honest description — no exaggerated claims, no hidden defects.

- Reply to inquiries with full disclosure on carrier, contract status, credit balance, and history.

- Negotiate one fair price. Do not bait buyers with a low quote and then raise it. Do not use false competing-offer claims.

- Meet the buyer at the carrier store the number is actually on — not a different store, not a coffee shop, not a parking lot.

- Hand over ownership through the proper transfer, receive payment in full on the spot, and provide a clean release.

Seller-side halal rulings

- Honest representation: if the number has been ported, has a history of spam complaints, or was previously associated with a defaulted contract, the seller must disclose it. Hiding defects is gharar.

- No price baiting: the listed price must be the price the seller is genuinely willing to accept. Quoting low to attract interest then raising the price at the store is a form of bay' al-najash (price manipulation) and is impermissible.

- No fake bidders: sellers must not invent competing offers to pressure a buyer. This is a deceptive practice in Sharia.

- Spot settlement: the seller should accept payment in full at the carrier store. Offering "split payments with interest" makes the deal riba-tainted on the seller's side.

If you are exiting the UAE and need to sell before departure, the timing logic in Leaving UAE? What to Do With Your Mobile Number covers the practical sequencing. If you are positioning to maximise sale value, the case studies in Can Your Phone Number Make You a Millionaire in Dubai? show the high end of the market.

9. The 786 premium tier — pricing, etiquette, who buys

The number 786 is the numerical abjad value of the opening Islamic phrase "Bismillah ar-Rahman ar-Rahim" (In the name of Allah, the Most Gracious, the Most Merciful). For many UAE Muslim buyers it is a respected, spiritually meaningful pattern — which is why 786 listings command a premium and trade in a specific etiquette.

2026 pricing bands

- Entry tier (AED 10,000 – 100,000): 786 appearing within a mid-tier prefix (055, 056), often as the middle three digits. Accessible for first-time buyers.

- Mid tier (AED 100,000 – 500,000): 786 in a premium prefix (050, 052) with clean surrounding digits. Strong long-term hold candidates.

- Collector tier (AED 500,000+): 786 leading a premium prefix with a repeating or sequential tail — for example 050-786-XXXX where XXXX is itself a repeat pattern. Scarce, trophy listings.

786 etiquette

786 numbers are typically held privately and listed by referral. Sellers expect serious, single-offer negotiations. Buyers should approach with respect, avoid lowball anchoring, and be prepared to move quickly once a price is agreed. Public auction-style bidding on 786 numbers is uncommon and culturally less welcome — direct private negotiation is the norm.

Who buys 786 numbers

- UAE-based Muslim entrepreneurs who want a spiritually aligned business line.

- Family heads acquiring a meaningful number to pass to children.

- Collectors who specialise in 786 patterns across multiple prefixes.

- Corporates branding a customer hotline with a number their Muslim customer base will recognise.

"Buy a 786 because it means something to you — not because someone told you it will double. Halal intent is the first filter."

10. Comparison table: Halal mobile number marketplace vs other halal-friendly assets

| Dimension | UAE VIP mobile number (also called a cell phone number) | Physical Gold | Halal Stocks (Sharia-screened) | Crypto (mixed view) |

|---|---|---|---|---|

| Tangibility | Yes — SIM + TDRA record | Yes — physical metal | Indirect — shares in real business | Debated among scholars |

| Interest exposure | None when paid spot | None | Must screen company balance sheet | Depends on the token model |

| Gharar (uncertainty) | Low — fully disclosed at carrier | Low | Medium — market-driven price | High — volatile, opaque |

| Liquidity | Medium — buyer-driven | High | High | High but volatile |

| Entry ticket (AED) | ~5,000 to 500,000+ | ~2,000+ | Any size | Any size |

| UAE-specific | Yes — locally regulated | Global | Global | Global |

| Scholar consensus | Generally accepted as tangible | Strong consensus | Strong with screening | Active debate |

The mobile number sits in a specific niche: UAE-local, tangible through the carrier registration, with low gharar when transacted properly. It is not a substitute for diversified halal investing — it is a UAE-specific alternative asset.

11. Common halal red flags to avoid

The following patterns are halal red flags. If you encounter any of them during a transaction, pause and reassess. None of these are minor — each one breaks the structural soundness of the deal.

- Installment plans with a premium: "Pay AED 5,000 a month for 12 months, total AED 60,000 — but the cash price would be AED 50,000." That AED 10,000 difference is structurally riba.

- Interest-bearing escrow: a service that holds funds and pays interest to either side. A flat service fee is fine; an interest mechanism is not.

- Vague seller identity: a seller who refuses to share their full name or Emirates ID details before the store visit. Gharar.

- Auction-style emotional escalation: being pressured to raise your bid because "another buyer is calling now". Maysir adjacent.

- Pre-payment with no transfer date: any request for payment before the carrier store visit with a vague "we'll transfer next week". Refuse.

- Hidden contract: a seller who fails to disclose that the line is locked into a postpaid contract with an early termination fee. Gharar.

- Off-channel meetings: requests to meet anywhere except an authorised carrier store. There is no legitimate halal transfer mechanism outside the carrier.

12. Frequently asked questions

Is buying a UAE VIP mobile number halal?

Buying a UAE VIP mobile number is structurally halal when the transaction satisfies four conditions: spot-cash settlement with no interest, full disclosure of the asset, tangible ownership transfer through the carrier (Etisalat or du), and TDRA registration in the buyer's name. The mobile number is treated as a usufruct attached to a real, regulated, transferable asset. Whether your specific situation is permissible depends on personal factors — consult a qualified scholar for a personal ruling.

Can I pay for a halal mobile number in installments?

You can pay in installments only if the total price is identical to the spot-cash price and there is no premium for delayed payment. Any "extra" added because the payment is spread out over time is structurally riba and breaks the halal compatibility. Spot-cash settlement at the carrier store on the day of transfer is the cleanest halal route.

Are 786 mobile numbers more expensive because they are religious?

786 numbers carry a premium in the UAE market because of the pattern's spiritual resonance with the Bismillah phrase in Islamic tradition. The premium reflects genuine demand from buyers who value the pattern. Pricing the asset based on its cultural and spiritual significance is permissible — what is impermissible is artificial price manipulation, fake competing offers, or interest-bearing payment structures around the sale.

What documents do I need for a halal mobile number transfer?

You need a valid original Emirates ID, the agreed payment ready (cash within store limits, or instant bank transfer), and you must visit a main Etisalat (e&) or du business centre — not a kiosk. The seller must also bring their original Emirates ID. The carrier operator will print and process the ownership transfer on the spot. No additional notary or legal documents are required for a standard personal transfer.

Can I use an escrow service for a halal mobile number purchase?

You can use an escrow service if it charges a flat service fee rather than an interest-based percentage on held funds. The escrow agent is providing a service (holding the money pending the transfer) and a defined fee for that service is permissible. An escrow that pays interest to either party, or that takes a cut linked to time held, is not halal-compatible.

How long does the TDRA ownership transfer take?

The carrier-store TDRA ownership transfer typically takes 30 to 60 minutes from arrival to new-SIM activation. Both parties must be present with valid Emirates IDs. The new SIM is provisioned on the spot. The new owner can use the number immediately after stepping outside the store.

What if the seller refuses to disclose the carrier or contract status?

Refusal to disclose carrier or contract status is gharar — the buyer does not know what they are buying — and breaks halal compatibility. Walk away. A legitimate halal-compatible seller will answer the four disclosure questions clearly: which carrier, ported or not, contract or prepaid, and outstanding balance status. Anything less and the deal is structurally unsound.

Is it halal to flip mobile numbers for profit?

Buying a mobile number with the intention of reselling at a higher price is permissible when the asset is real, the resale price reflects market demand, and the seller follows the same halal procedure on the way out. Sharia scholars generally accept reasonable resale intent on tangible assets. What is not permissible is artificial cornering of patterns, market manipulation, or interest-based financing of the inventory. Allahu A'lam.

Can a non-Muslim sell a halal-compatible number to a Muslim buyer?

Yes — the halal compatibility of a transaction depends on its structure, not on the religious identity of the parties. A non-Muslim seller who follows the five-step process (honest listing, full disclosure, one fair price, carrier-store meeting, spot settlement) is providing a halal-compatible deal to the Muslim buyer. The buyer's responsibility is to ensure their own side of the transaction satisfies the principles.

What happens if the SIM is suspended after I buy it?

A SIM can be suspended after purchase if there is an unpaid balance the seller did not disclose, or if the line had a regulatory flag the carrier did not surface at transfer. To protect yourself, get a printed carrier confirmation of "no outstanding balance" on the day of transfer, keep the transfer receipt, and verify the line is active before leaving the store. If a problem surfaces afterward, the TDRA consumer complaint channel and the carrier's customer protection desk are the resolution path.

Ready to act?

Browse current halal-compatible listings or list your own number with full disclosure.

Browse VIP numbers List your number Estimate your number's valueSources & references: TDRA (tdra.gov.ae) consumer regulations; AAOIFI Sharia standards on tangible asset transactions; Emirates Auction public mobile number sale records. This article provides structural framework only and is not personal financial or religious advice.